Tiny ASX Company in Race to Discover the ‘Australian Andes’

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Andes – It’s one of the most valuable and lucrative mining regions in the world. Rumours and whispers have been heard around mining circles for decades about an undiscovered potential “Andes equivalent” based right here in Victoria, Australia. Legend has it that beneath the rolling farmland, lies significant tonnes of copper – and a fair bit of gold too. So when we heard that Stavely is trying to discover and prove up this Victorian equivalent to the Andes, and is going to IPO at almost $18 million on the ASX in a few weeks, we started doing our research about making an investment... And what we researched shocked us! We were alerted to an ALREADY LISTED hidden gem doing the exact same thing in the exact same area – that offers a discount of almost 10 times than that of the $18 million IPO. Compared to the Stavely IPO opportunity, this tiny ASX listed company has:

- More Land

- More Confirmed Mineral Bodies

- Bigger List of Targets

- Bigger Strike Lengths of prospective rocks

But the most startling thing – this company is so far under the market’s radar that it’s currently valued at only $2.4 million! Don’t you just love it when you buy something, and then see it advertised later for way more than you paid? Although this company is currently valued at $2.4 million, we expect this valuation to change dramatically in the next few weeks following the success of Stavely’s IPO (a value of almost $18 million) and subsequent listing on the ASX. After the Stavely IPO closes on April 23 rd – Watch out for the rerating of our tiny $2.4 million quiet achiever, especially with the amount of energy that is spent promoting IPOs to the market. At the Next Small Cap we look out for the little guys – backing companies under the radar and temporarily overlooked by the market – and this little company fits the bill. In the small cap game it’s extremely high risk investing but high rewards are possible. The tiny, unknown company has twice as many red metal prospects as Stavely, the new big kid on the block. Think about that – our pick has four high value targets compared to two. Its tenements completely surround Stavely. They have more than double the land. And it is at least equally or possibly more prospective. The tiny company is a first mover in a mining region in Victoria that’s only just been opened up to exploration and it has over a thousand square clicks of prime prospecting land in the bag. Word is the region could yield massive deposits of copper – comparable to The Andes in South America – one of the richest mining regions on the planet! That’s why State and Federal governments are falling over themselves to fund drilling programs in the region. Initial drilling results have just been released – with signs pointing to shallow copper and gold with unlimited depth potential – it won’t be long before the market cottons onto this company. Stavely’s IPO offer will close in just a few weeks. This should see Stavely worth as much as $18 million. We believe there is a narrowing window of opportunity to get into this tiny company while it’s still worth just $2.4 million. The Next Small Cap works hard to secure LONG TERM holds in companies with hot potential and we’re pleased to introduce our latest addition:

Navarre Minerals (ASX:NML) is based in the little western Victorian town of Stawell where The Stawell Gift, Australia’s oldest and richest running race is held every year. The winner of that hundred and twenty metre dash pockets a cool $40,000. But that’s chump change compared to the millions of dollars NML is chasing in an emerging copper belt near to Stawell called the Miga Arc just 250km northwest of Melbourne.

NML is racing for a bigger prize money than these guys

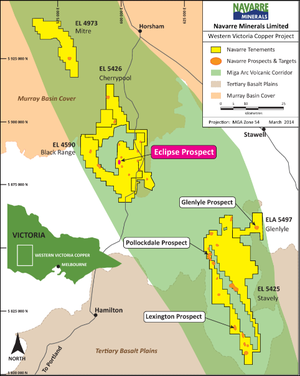

Geology surveys of the Miga Arc by the Victorian government have shown this once volcanic land formed in a similar way to The Andes in South America where huge mineral deposits known as porphyries are as common as altitude sickness. NML saw the potential in the Miga Arc before anyone else and snapped up 100% ownership of 1,278km 2 of it – a dominant position – containing four copper porphyry prospects. NML is exploring for porphyry copper deposits with a target size greater than 300Mt tonnes with copper grades in a range of 0.3 – 2% and gold from 0.3 – 2 g/t. The Miga Arc’s potential is enormous. It’s similar to the widely explored Macquarie Arc in central NSW where there are six established mines digging up lots of copper and gold which includes the monster Cadia copper and gold mine near Orange. But the race there’s been run. The Miga Arc has NO established mines and is only just being opened up by first movers like NML. NML calls its holdings in the Miga Arc The Western Victoria Copper Project and of its four prospects, its main effort right now is at a prospect called Eclipse, one hour drive to the west of Stawell. At Eclipse, NML is working to prove the size and make up of this confirmed copper porphyry prospect by exploring three targets in close proximity including a shallow blanket of minerals at only 30 metres depth.

NML is moving fast. They just released results of the initial drilling programme , and all signs point to the presence of Victoria’s first copper-gold porphyry. It’s likely that NML will need to raise some more funds – so it can drill even deeper and hunt down the porphyries within its portfolio of assets. If NML proves its first porphyry (one of four areas it has) it may no longer be a $2.4 M company – investors have a rapidly closing window of opportunity to get in at the ground level. Remember, Stavely Minerals are operating in the same area and about to IPO – valuing that company at $18M. Stavely’s worth seems largely driven by the mineral resource it has in the Miga Arc – a shallow secondary copper blanket, plus one modest inferred resource at its Ararat VMS project and $5M cash on IPO – no guesses why we’re backing the undervalued NML! The starting gun has been fired in the Miga Arc and we are backing NML to take the ribbon. In this article The Next Small Cap will explain: – What porphyries are and why the Miga Arc may just be an Aussie version of the mineral rich Andes – NML’s clever plans for the Miga Arc and why its position there is so dominant – NML’s drilling programmes and its plans for the future Strap yourselves in – NML is moving fast and the race goes to the swift.

Our Track Record:

Did you catch the Next Tech Stock ’s latest release on AnaeCo (ASX:ANQ) ? ANQ has traded as high as 160% since:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

NML and Stavely Minerals – Advancing the Aussie Andes

An unlisted junior exploration company called Stavely Minerals is currently raising $6 million and gearing up for an IPO on the ASX. From the number of shares available at 20 cents each, they are looking at an initial market cap of between $15 million and $18 million. Remember NML is only capped at $2.4 million . Stavely were recently featured in the Australian Financial Review :

![]()

... and the Australian :

Stavely even got a front page yarn in Australia’s Pay Dirt :

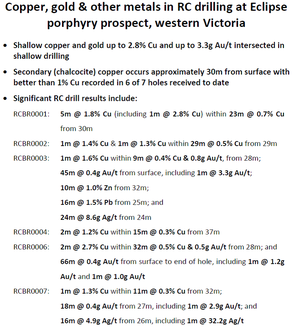

Why the big buzz? Stavely has compelling indications of deeper porphyry (not yet confirmed) including a modest secondary copper inferred resource of 28Mt at 0.4% copper for 110kt of contained Cu. NML’s new drilling results indicates it has similar shallow secondary copper too! The one inferred resource, another modest inferred resource at its Ararat VMS project, and $5M cash on IPO gave Stavely something to excite the market with and its current heading towards an IPO with a minimum company valuation of $15 million. Great news for the Miga Arc – the more action the better for all players. Stavely and NML are roughly similar, operating in the same areas and have similar plans. The vital stats of both companies shows NML has equal if not more potential due to its land footprint, and its long list of targets however NML is significantly undervalued . Let’s go into more detail and compare both companies objectively.

Mineral resource and size:

NML 0 vs Stavely 1

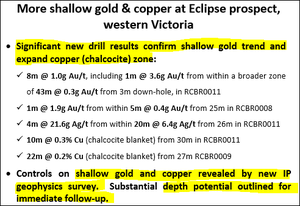

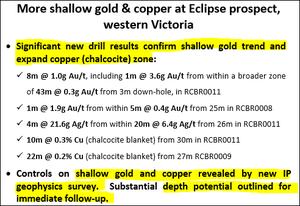

Stavely wins the first round – laying claim to an inferred shallow resource blanket of 28 Mt @ 0.4% Cu, for 110 kt of contained copper. Just the stuff to show there could be something bigger at depth. Whilst NML can’t lay claim to an inferred resource just yet, their latest drill results show that they have the same shallow secondary copper blanket too (with added gold) – it just requires further step out drilling. NML are well on their way, as evidenced by the drilling programme in full flight. Recent drill results by NML were particularly encouraging:

Now the Government is sniffing around and viewing the region as high potential and something to improve the economy, NML may just get a free drilling kick very soon – with the amount of land NML are sitting on, the Government is likely to do some work for them.

Porphyry Prospects:

NML 4 vs Stavely 2

NML wins this round. NML has four porphyry prospects that it’s working on – Eclipse is the most advanced. Stavely has two in the region but to be fair, they’ve not done much field work there yet.

NML has 4 targets: Eclipse, Glenlyle, Pollockdale and Lexington

We believe NML has a greater chance of success with 4 porphry targets.

Mineral Targets:

NML 80 vs Stavely 11

Another convincing win for NML. Both companies will be drilling like mad but again NML has the upper hand here. Stavely has 11 targets at its two prospects. NML has 50 targets to work up and drill. 26 of these are near their Eclipse prospect whilst the remainder are at its other exploration sites near Stavely.

Total “Andean” Footprint:

NML 1,278 km 2 vs Stavely 629 km 2

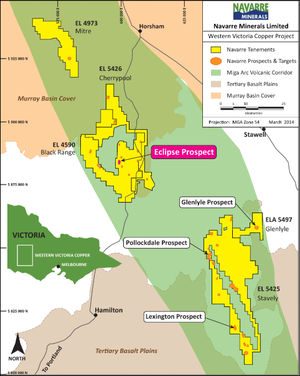

The fact that NML has more targets is helped by the fact they have much more land in the region than Stavely. NML holds 1,278km2 compared to the 629km2 held by Stavely. Total land is important because porphyry deposits occur in clusters – you find one...you find several others nearby. NML’s large tenement holdings means it can explore more of the mineral rich Miga Arc region in the future and expand its operations. The yellow land in the map is all NML’s. If you look to the southern chunk of NML land, you will see a green shape in the middle – that’s Stavely’s main licence.

Land in strike length:

NML 140km vs Stavely 62 km

NML has 140km of volcanic strike length of the prospective Miga Arc while Stavely has 62km. That’s more than twice as much!

Land in the volcanic strike length of the Miga Arc has a higher chance of containing a porphyry – NML’s holdings have more territory in the money zone.

NML’s back yard

An advantage for NML is its local status – its head office is only one hour’s drive from its Miga Arc properties – a distinct advantage when exploring.

The NML team: Friendly locals with a desire for success

Stavely has had some early success by proving-up one of its two prospects in the Miga Arc. It will also have $5 million cash on completion of the IPO. Whilst NML are currently running low in funds, The Next Small Cap is still backing NML – it has more land in the money zone, 4 porphyry prospects, lots of targets and a local work force, who live and work in the communities they explore. And it comes a lot cheaper – NML’s market cap is just $2.4M, while Stavely are listing for $18 million . Whilst Stavely do have other projects, it still values their Miga Arc project much, much higher than NML. At The Next Small Cap we like to do our research – we are backing the cheaper, discounted version of the two.

Our Track Record

Did you receive The Next Small Cap report on Segue Resources (ASX:SEG)? Since this report was released, SEG has been up as high as 130%.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The Miga Arc – a porphyry playground

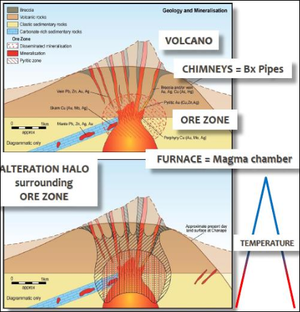

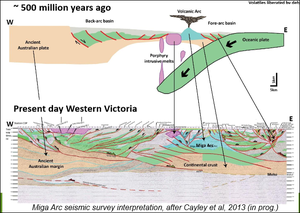

It sounds like a 1980s computer, but The Miga Arc is a geological formation that really has the potential to create a lucrative mining region. It’s comparable to the mineral rich arcs found in the Andes in South America – where most of the world’s copper is mined from. The reason for the excitement is one word – porphyry. What is a porphyry? In a volcanic area with lots of magma, different metals can pool together as the area cools – creating huge deposits of things like copper and gold and tungsten. Those big lumps are called a porphyry.

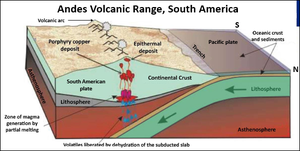

Most porphyries are large, low-grade, bulk mined deposits. The largest can be between 1.3 to 3 billion tonnes! Just finding one porphyry allows a mining company like NML to set up shop for a long time and exploit a huge deposit. You may recall another Next Small Cap company chasing porphyries – they’ve just started drilling in the Andes – Promesa (ASX:PRA) Why is NML targeting the Miga Arc? The Miga Arc is geologically similar to The Andes, the mountain range stretching across South America from Venezuela to Argentina. It’s just a few tens of millions of years older, so the Victoria version is hidden from sight. Forget mountains though – the similarities are below the surface!

Victoria’s Miga Arc is in a very similar continental setting to The Andes. It runs along an ancient tectonic plate boundary where there were active volcanoes 500 million years ago.

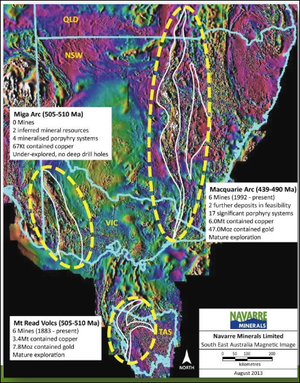

All that volcanic activity left concentrations of minerals in the ground like peanuts in a chocolate bar! The biggest deposits of copper porphyry in the world are found in the Atacama Desert at the edge of The Andes between Chile and Peru – both are the largest exporters of red metal in the world. If the Miga Arc can yield even a fraction of the copper found in the Andes, it will be a very busy mining region for a long time to come. Drawing analogies closer to home, geological surveys have shown the Miga Arc is similar to the widely explored Macquarie Arc in central NSW where there are six established mines digging up 6.0Mt of contained copper and 47.0Moz of contained gold. There are 17 significant porphyry systems in the Macquarie Arc alone . The Miga Arc Victorian belt has had little to no exploration activity over the years.

Also, the Miga Arc’s rocks are similar in age and type to the Mt Read Volcanics found in Tasmania which supports copper mining mainly at Mt Lyell which yields copper and gold. These proven and lucrative Australian mining areas make the similar ground of the Miga Arc a high potential region.

Our Track Record:

Did you catch The Next Oil Rush ‘tip of the decade’ – TSX:AOI back in February 2012? The Next Oil Rush called it at around CAD$1.8 and has been as high as CAD$11.25 since – that’s over 600%!

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

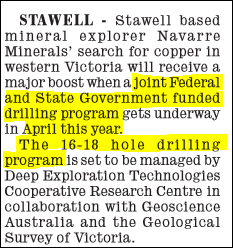

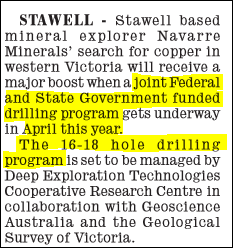

Government Run Multi-Million Dollar Drilling Campaign

In efforts to revitalise the states flagging economy, the Victorian government has been doing a lot of grunt work in exploration in the region. Ground traverses by the Victorian Department of State Development, Business and Innovation’s Geological Survey have discovered the volcanic rocks in the region – aiding the selection of porphyry targets. Now, the government is funding a multi-million dollar drilling campaign in the region – drilling 16 to 18 holes.

Based on NML’s large land holdings and highly prospective land, a couple of holes are bound to fall onto NML land – that’s free drilling, no strings attached! The Government is investing so much cash in the region in order to boost the economy – if they can help out little explorers like NML and find some big deposits – it will mean millions of dollars in returns to the state’s coffers – and boosting the region with more jobs and an improved economic outlook. The infrastructure is there, they just need someone like NML to confirm something big.

NML’s Victorian porphyry plan

NML purchased a huge swathe of land in the Miga Arc – over 1,200km 2 of land with 140kms within the Miga Arc’s volcanic strike length – the money zone where there’s a higher chance of finding multiple porphyries. Right now, NML has four main Cu-porphyry prospects – Eclipse, Lexington, Pollockdale and Glenlyle.

NML calls its huge holdings in Western Victoria ‘the big footprint’ and its master plan is to prove as many of the porphyry deposits as possible and then develop a plan to mine them. Yes, that’s Stavely’s thin slice in the middle of the southern tenement. NML’s holdings are close to infrastructure such as roads, rail, power and a skilled local workforce based at Stawell. Victoria has been in the mining business since the gold rushes of the 1850s so a few extra deposits of copper won’t hurt!

![]()

NML’s Managing Director Geoff McDermott told The Wimmera Mail-Times , a newspaper in the region, that one of his company’s best advantages is that they are local. ‘Should a potential mine be found, we could harness the skills developed over the past 30 years around Stawell and put them to good use rather than having people go off to other industries,’ he said. When the time comes to mine its monster deposits of copper, NML will be a magnet for skilled workers eager to help it succeed in their own backyard.

Our Track Record:

Did you see The Next Oil Rush report on Swala Energy (ASX:SWE)? SWE has traded as high as 150% since:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

NML’s Red Metal Race at Eclipse

Let’s get down to brass tacks, or maybe copper ones would be more appropriate? In January of 2014, NML announced it had begun a Reverse Circulation (RC) drilling programme at its Eclipse copper-gold porphyry prospect, part of its Western Victoria Copper Project in the Miga Arc.

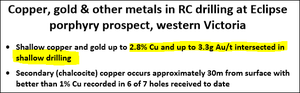

NML just release their initial drilling results, laying out strong evidence for primary porphyry copper mineralisation at depth:

To confirm the size and shape of the copper porphyry it’s drilling into what’s known as a supergene blanket of secondary copper and gold usually found above the bigger deposit.

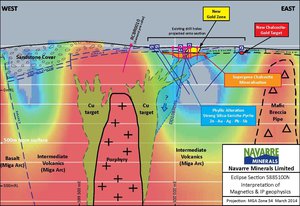

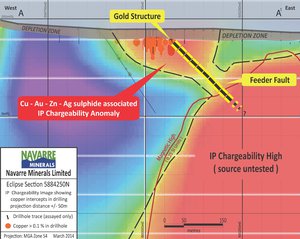

Now that NML has confirmed the existence of a supergene blanket at shallow depths, the company is now searching for the big kahuna porphyry deposit below it. It doesn’t look too far away given NML’s latest ASX announcement . The supergene blanket is linked to a larger target just below by a feeder fault – could this just be the elusive porphyry they have been searching for? The diagram below shows a cross section showing the shallow supergene copper linking to a monster target just a bit deeper. As you can see, many drills have been done in the area, just look at the deep drill from the 1980s – quite the near miss! If they had have moved the location slightly to the east this might already be a producing mine.

Now NML plan to move forward in their exploration and will undertake further drilling – with the ultimate plan of a deep diamond drill program to hit its copper-gold porphyry targets. The Next Small Cap will also be keeping an eye on the government’s plans in the region – NML could get a helpful boost through a couple of free drills – watch this space. NML are proving up their targets fast, and remain particularly overlooked in the marketplace – at just $2.4 million market cap they represent serious value for money.

Our Track Record

Did you receive The Next Small Cap report on Core Exploration (ASX:CXO)? Since this report was released, CXO has been up as high as 80%.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The track ahead for NML

Stavely is about to IPO for at least $15 million with ONE confirmed resource in the Miga Arc and just over 600km2 of land. The market will know the true value of NML once Stavely closes their IPO offer and lists on 7 th May 2014. Strong potential for a re-rate of NML is possible on the back of this IPO. NML has FOUR porphyry prospects under exploration and more than a thousand square clicks of land. That’s four good chances to strike pay dirt with more to come. NML is moving fast in 2014. Initial drill results were just released and encouraging signs continues to appear. Part and parcel of tiny companies like NML, we expect to see a capital raise in the coming months. NML will use any additional cash to undertake further drilling – with the ultimate plan of a deeper diamond drill program to hit those copper-gold porphyry targets. Now with a supergene blanket of copper confirmed – the same as Stavely, NML will plan to drill even deeper to the copper porphyry below and see how big and shiny the metals are. The next few months should be interesting – no doubt the majors will be watching the region, ready to pounce should NML deliver on the porphyry. The Next Small Cap will also be watching where the government plans to drill in their multi-million dollar campaign in the region. NML remain particularly overlooked in the marketplace – at just $2.4 million market cap they represent a solid discount and serious value for money when compared to Stavely – about to list for over $15 million. When the Stavely IPO closes on April 23 rd ... NML investors should strap themselves in. Don’t forget to like NML on Facebook – or follow them on Twitter .

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.