Path Cleared for ERL’s WA Gold Production: Begins Next Quarter

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

We’ve kept track of a host of gold juniors marching to market in recent months, as gold prices have bounced back to favourable levels, and previously uneconomic projects have suddenly become attractive for development once again.

Empire Resources (ASX:ERL) has assembled a straightforward gold mining strategy that includes working with the likes of the $179M capped mining contractor NRW Holdings (ASX:NRH), who will undertake all open pit mining operations at ERL’s Penny’s Find gold mine.

Under the terms of the agreement , ERL will now have sufficient funds to conduct mining activities through to the start of gold production.

Penny’s Find is a JV project between ERL and Brimstone Resources, with ERL holding the 60/40 split in its favour.

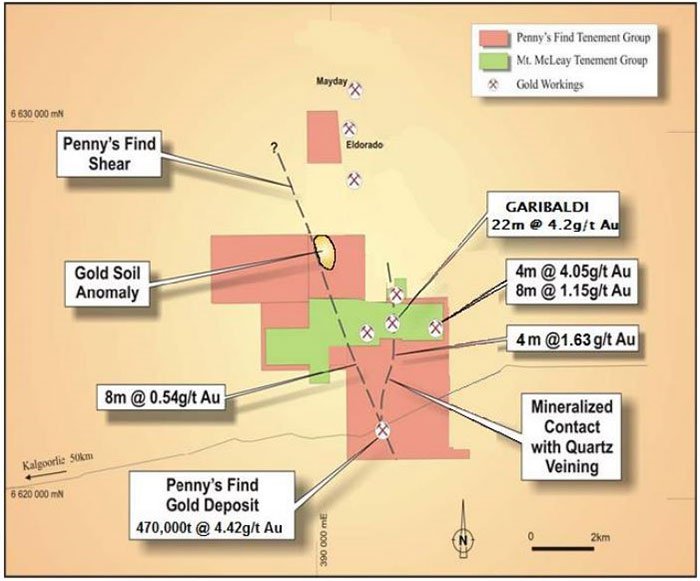

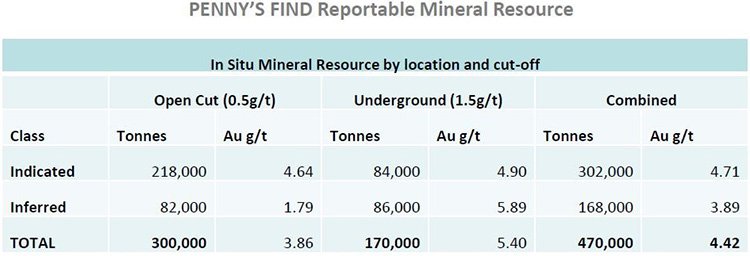

The Project contains a 470,000 tonnes @ 4.42g/t gold resource and has thus far delivered shallow high-grade gold from initial samples and has an open-pit mine in construction stage.

Yet it is still an early stage play and therefore investors should seek professional financial advice for further information if considering this stock for their portfolio.

Interestingly the road that runs through the pit is currently being realigned and is only days away from completion. The Kurnalpi-Pinjin Road ran over the open-pit location, meaning the road had to be rerouted before digging could commence.

An Underground Feasibility study is also underway to supplement ERL’s existing Bankable Feasibility Study (BFS) based on the open pit.

The total cost of production , which sits at AU$1,086/oz. according to the BFS, is believed to generate revenues of between AU$29.6m- AU$33.6m in the first year of full production. If all the cards fall in place the company could be cash-flow positive within eight months and generate $7.6M in free cash flow in less than a year, with every AU$100/oz. increase in the gold price above AU$1,500/oz. leading to an additional AU$2 million in free cash flow.

The good news for ERL is that the project is now in the final straight before production commences sometime next quarter.

It’s most recent achievements to date include:

- A crucial road re-alignment on time and budget (scheduled to be completed in days)

- Site earthworks completed for laydown area for site offices and workshops

- Site earthworks completed for a dewatering dam and water supply.

With project development at an advanced stage and results coming down the wire over the coming months; claiming a stake in this ‘Empire’ could be just what the bank manager ordered.

Keeping track of:

![]()

Empire Resources (ASX:ERL) is a junior gold explorer that’s walking a path to gold production in the very near term and taking advantage of macro gold economics.

Grabbing a share of the lucrative gold market is no easy feat. As precious metals aficionados know, gold is a precious metal with a very limited supply.

Despite suffering a lot of market volatility in recent years, the yellow metal is back loitering at price levels that are conducive to strong cash flow.

Take a look at gold prices, as measured in Aussie dollars:

This year has been a good year for gold despite the volatility — having started the year at around AU$1,500/oz., spot gold prices reached an all-time high of AU$1,857 in June.

At the same time, like all commodities, we should point out that the gold price can also go down just as easily – always take a cautious approach to any investment in any gold stock.

This year Aussie gold miners have done pretty well:

With the pullback now at a crucial phase, laying down some strategically-placed stakes in junior gold miners such as ERL might be just the way to go...

...as gold continues to find support and remains on a gradual up-trend.

The HUI Gold Index has finally found a bottom and has been clawing back losses made since the GFC.

If ERL succeeds in bringing in its first revenues from its flagship Penny’s Find gold project near Kalgoorlie, it could set the stage for ERL to continue its own development by providing cash flow for further exploration or to acquire other gold projects.

Either way, ERL could be on track for a higher valuation as it tracks toward production.

With most Resources plays — the devil is in the detail, or in the case of ERL, its gold project has some features that could well put ERL ahead of other gold juniors in the area.

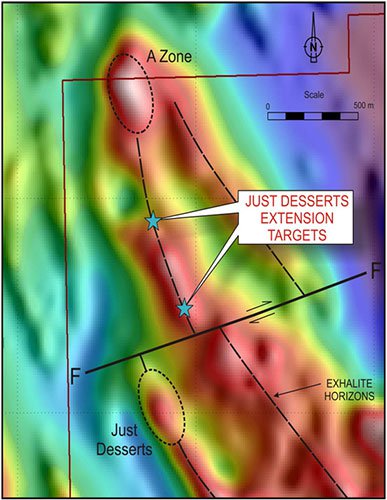

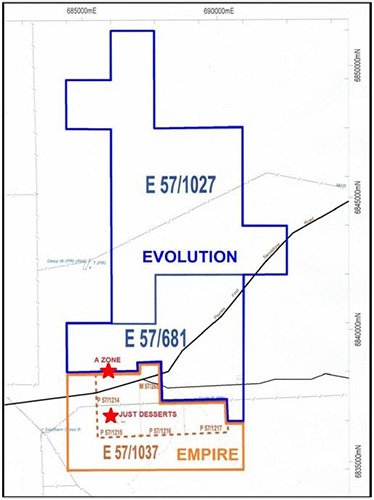

Let’s take a look at the real estate this Empire commands

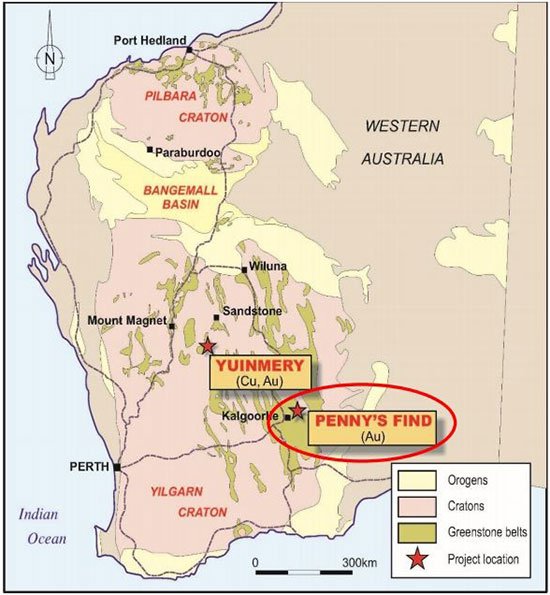

ERL is operating in WA — in and around the world famous gold fields surrounding Kalgoorlie and Coolgardie. Here is ERL’s Penny’s Find Project location on the map, sitting north east of Kalgoorlie:

If ERL can produce gold in this part of Australia, Penny’s Find could be a superb revenue driver for ERL’s early development.

Currently, ERL is the operator of Penny’s Find on a 60/40 JV deal with Brimstone Resources, and will therefore reap the lion’s share of the spoils once this asset goes into production next year.

High-grade and near-term

All gold explorers are generally looking for two things: quantity and grade.

ERL’s Penny’s Find has already shown shallow high-grade gold from initial samples, with an open-pit mine currently in the construction stage.

Then there’s additional underground potential with a Feasibility study now underway to supplement ERL’s existing Bankable Feasibility Study (BFS) based on the open pit.

Here are some of the most recent results received by ERL:

The first round of RC grade control drilling at Penny’s Find was done in Q2 2016 with 86 holes drilled for 2,534 metres completed.

This is the first of three grade control programmes scheduled in the planned 80 metre deep open pit.

The programme was designed to better define the position of the gold zone from surface to approximately 30m depth and to increase confidence in the early mining phase.

Let’s have another look at this Penny to see what’s involved, and more importantly, what luck it could bring for this ‘Empire’

ERL’s first drilling efforts have been upbeat.

Grade control drilling is returning relatively strong results while intersections at shallow depths have exceeded expectations.

That’s the kind of early-stage result we look for here at The Next Small Cap — strong early hits, plenty of drilling already done, and most importantly...

...production to kick-off in the very near term.

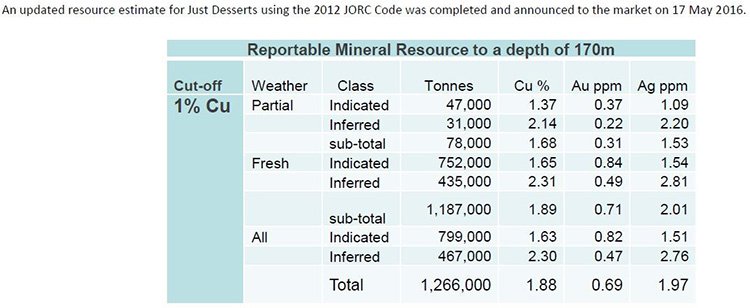

One other excellent feature is the fact that ERL’s Penny’s Find already has a BFS completed, which means investors are not jumping into the unknown.

On the contrary, ERL shareholders have a stake in these independent estimates:

ERL can boast a sturdy 470,000 tonne Resource that’s then bolstered by an efficient cost schedule which stands as one of the most competitive in the industry.

ERL is able to extract its ore at around $140 per tonne, and has an assumed recovery rate of 93%.

Initially the ore will be treated by Golden Mile Milling which operates the Lakewood Mill located on the outskirts of Kalgoorlie, 63km from Penny’s Find.

A Memorandum of Understanding was signed with Golden Mile Milling for the toll treatment of the ore, and this deal is expected to generate ERL’s first sales revenues.

Processing the ore through Golden Mile will enable ERL to become one of the most efficient junior producers in the local area, and estimates seen so far suggest ERL will be paying approximately $45-$50 per tonne.

Overall, ERL’s total cost of production is AU$1,086/oz. which according to ERL’s BFS, could generate revenues of between AU$29.6m- AU$33.6m in the first year of full production.

If all goes to plan, ERL is on track to achieve cash-flow positive status within 8 months.

So just to get the story straight

ERL has access to a Gold Resource of 470,000 tonnes @ 4.42g/t...

...is profitable with gold prices at ~AU$1,500 while current gold prices trade at around ~A$1,650 and rising...

...is about to go into production in early 2017...

...and yet, this nugget-excavator remains valued at just $14M?

This could be a case of a shiny junior getting lost in the nooks and crannies of global gold exploration currently dominated by the gold mid-caps and majors.

If so, ERL could be approaching a moment of market discovery, and hopefully some northward price movement.

Here’s how ERL shares have performed so far this year — is the market gradually waking up to this embryonic gold player?

Of course, avid Next Small Cap readers would have no doubt got the message about ERL back in August of this year, when we released our first article on the stock .

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Penny’s Find BFS estimates that ERL could generate $7.6M in free cash flow in less than a year with every AU$100/oz. increase above AU$1,500, leading to an additional AU$2 million in free cash flow.

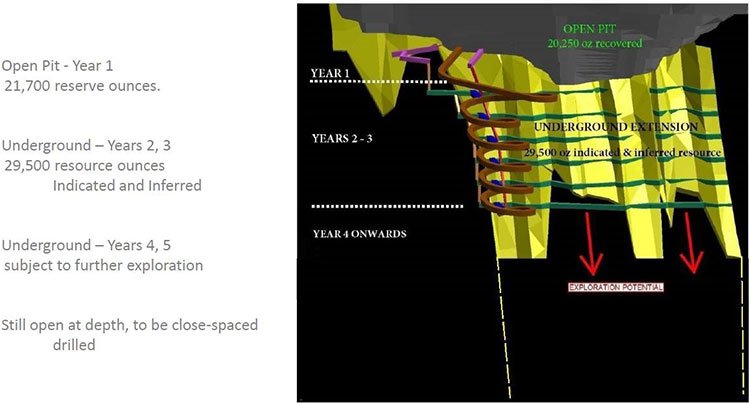

Going underground

ERL is working to eventually take the mine underground as Penny’s Find’s gold mineralisation extends to at least 250m depth where it remains open with a current known deeper resource inventory of 170,000 tonnes @ 5.40g/t Au beneath the open pit.

ERL has launched Feasibility studies to see how economic this gold that lurks beneath really is. Given historic comparisons, there is no good reason why ERL cannot add to its overall Resource by doing additional mining at greater depths.

This is one factor that could give this Empire a strong boost in the territorial stakes sometime in 2017/18, and would likely serve as a strong price catalyst if ERL were to prove up something significant below 250m depth.

The picture above shows ERL’s planned open pit (shown in yellow) with red blocks indicating high-grade gold mineralisation.

Further down at depth however, there is a possibility of higher-grades and larger quantities of ore.

This is how ERL’s preliminary design of its underground mine looks like:

Mine site infrastructure under construction

As part of its development work to get Penny Find into production, ERL has done a deal with NRW Holdings (ASX:NWH) to ensure Penny’s Find makes it to market without any last minute hitches.

NWH will construct an open-pit mine and assist with development in exchange for a 9.5% royalty from eventual sales.

Here is a mock-up of the mine site, developed by ERL and currently in construction.

Giving up a slice of the spoils in exchange for logistical security is a reassuring step because it means ERL is now fully funded to first production at Penny’s Find.

Incidentally, here is how NWH’s shares have performed so far this year — up 470% since February 2016 which could be a good indication that Aussie gold mining activity is picking up steam:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Building an Empire in Gold

ERL is a standout junior.

How many other junior gold explorers do you know that have a BFS done and dusted, a gold project with both open pit and underground gold resources reaching as high as 470,000oz in total, and possibly most price-sensitive — ERL is about to kick-start production aiming to net at the higher end of the range of A$2 million – A$7 million in free cash flow in 2017.

The company’s first revenue targets are now in sight and its Penny’s Find mine is in final preparation to start gold production early next year.

Yet this still remains an early stage play, so caution is advised if considering this stock for your portfolio.

When you consider that over the past decade, gold priced in both US and Aussie dollars has done this:

...it is not a surprise to see gold miners (especially in Australia) rushing off for their shovels.

Not only has ERL got all its gold-revenue-bearing factors nearly in duck-formation, it also has strong support from its partner (NWH) and maintains veteran expertise in the form of its Managing Director, David Sargeant. ERL’s MD has worked with major internationals such as the $23BN-capped Newmont Mining Corp and the $20BN-capped Esso.

ERL is yet another example of a small-cap junior making a strong case to become a market darling, as long as it can keep progress moving along at its Penny’s Find project in WA.

All the key factors have come together pretty nicely for ERL — a stalwart junior with an armoury of factors to begin its empire-building mission in WA as early as Q1 2017, and possibly imperialising the entire Aussie gold junior space in the years to come.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.