Major Upgrade for POW’s Vanadium Resource at Daejon

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

South Korea-based ASX explorer Protean Energy (ASX:POW) has revealed a significant upgrade to the vanadium/uranium mineral Resource estimate (MRE) for its Daejon vanadium/uranium project in Korea.

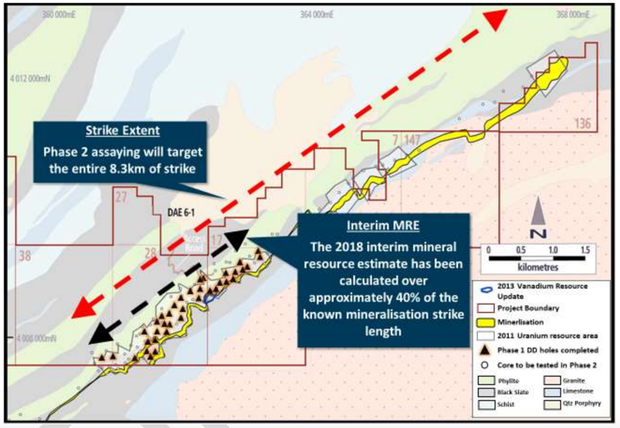

POW has estimated an interim vanadium/uranium mineral Resource across 40% of the known Daejon strike length, representing a significant increase to the existing JORC 2004 vanadium Resource.

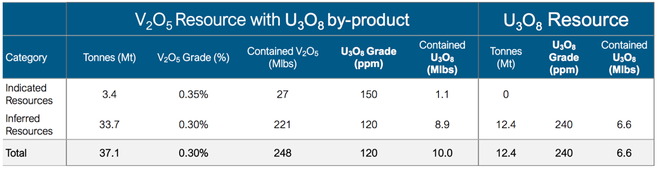

The resulting combined JORC (2012) compliant Mineral Resource Estimate now stands at 37.1 Mt at 3,000ppm vanadium (2,000ppm cut-off) and 120ppm uranium defined for a total of 248 Mlbs vanadium and 10 Mlbs uranium.

Specifically that’s: Indicated at 3.4 Mt at 3,500ppm vanadium and 150ppm uranium, and Inferred at 33.7 Mt at 3,000ppm vanadium and 120ppm uranium.

To put this in perspective, POW’s existing MRE for vanadium — its main focus — was 17.3Mlbs (largely Indicated) grading 3,186ppm V2O5 at a cut‐off of 2,000ppm V2O5.

To save you doing the maths, that is a difference of 230 million pounds... and a huge milestone as far as POW’s vanadium ambitions go.

This major news comes just weeks after POW’s announcement that it had successfully completed Phase 1 of the comprehensive portable-XRF calibration and assaying program being conducted at the Daejon deposit.

POW is developing the multi‐mineral Daejon Project through its 50% holding in Stonehenge Korea Limited (SHK). SHK owns 100% of the rights to three projects in South Korea — the flagship Daejon Project, plus the Gwesan Project and the Miwon Project.

It does remain a speculative stock, so investors should seek professional financial advice if considering this stock for their portfolio.

While it’s safe to say the company should be very happy with the results, we doubt it would be too surprised. In the 1970s and early 1980s the Korean government focused their exploration efforts on uranium mineralisation and completed a total of 36,000 metres of diamond drilling.

However the drill core was not systematically assayed for vanadium. And since where there’s uranium, there’s often vanadium, POW smelled an opportunity...

With even more confirmation that the team is onto a rich source of vanadium, the company’s news from June is even more promising. The small cap announced the installation of a 25kW (100kWh) V-KOR vanadium battery at the site of OzLinc Industries in O’Connor (Perth, Western Australia).

Through its holding in Stonehenge Korea, POW owns a part share of battery factory in South Korea that could see it have an end-to-end production to processing pathway for energy storage batteries. The vanadium batteries being made at the factory are called V-KOR, as mentioned above.

POW previously secured a $120,000 grant to fast-track the development and testing of its V-KOR range of vanadium redox flow batteries, specifically the 5kW/100kWh vanadium V-KOR battery being trialled in Western Australia.

The company provided an update in mid-June regarding an extensive testing program carried out on its 5kW and 25kW V-KOR vanadium battery units, reporting that over 3,000 cycles have now been tested on the 5kW stack, representing in excess of nine years of full daily cycles for a typical solar photovoltaic (PV) application.

Crucially, both units reported no significant degradation in performance. This testing supports that the batteries can meet ‘in use’ performance metrics, and the company considers this milestone a key step in its progression towards the commercialisation of V-KOR and customer orders.

There is plenty to catch up on, so without further delay, let’s check in with:

We should’ve guessed that the aptly-named POW could pack a punch... because that’s exactly what it did with this week’s news.

POW has announced a significant upgrade to the vanadium/uranium mineral Resource estimate for its South Korean Daejon vanadium/uranium project, reporting 240 million pounds V2O5.

The company now has a combined JORC (2012)-compliant MRE of 37.1 Mt at 3,000ppm vanadium (2,000ppm cut-off) and 120ppm uranium defined for a total of 248 Mlbs vanadium and 10 Mlbs uranium (tabled below).

It now also has an Estimate across 40% of the known Daejon strike length.

Not only that, but the strike length at Daejon could be set for a further extension.

Phase 2 is targeting the remaining 60% of the deposit strike length, and is expected to be completed imminently, resulting in a further Resource update.

It’s worth adding that the Daejon shale hosted deposit is similar in nature to the neighbouring Chinese “stone coal” deposits, which display grades ranging from 0.13% to 1% vanadium pentoxide.

Why does this matter? Well, stone coal vanadium deposits represented approximately 47% of the world’s vanadium production in 2017, and are the world’s primary source for the high purity vanadium electrolyte used in electricity storage applications.

Not to mention Chinese stone coal deposits are amenable to beneficiation processes, including selective flotation and magnetic separation methods, which are being successfully used to achieve an average 300% upgrade.

What led this micro-cap to such a POW-erful position?

For such a small market capitalisation, POW has secured an enviable position for itself as a junior metals play.

In 2011, SHK completed a Mineral Resource estimate (MRE) at the Daejon uranium project, using historical data. To date, only non-destructive testing methods have been permitted for the core stored at KIGAM.

In 2013, SHK drilled five holes which were assayed for uranium and vanadium, providing additional data for an update for the uranium MRE, and a maiden vanadium MRE in a restricted area around the 2013 drilling.

The company then set out to prove the feasibility of using portable XRF (p-XRF) devices to collect analytical data from core in a 2017 orientation study using the 2013 core and assays... which brings us to January this year, when the company commenced a p-XRF testing program of the core at KIGAM.

This included a significant element of quality control testing to really demonstrate that the technique was suitable for the job.

Through all that, it successfully demonstrated that the sample and analytical precision as well as analytical accuracy was enough to support Indicated and Inferred Mineral Resources at Daejon — and so here we are, with this week’s big news.

Latest MRE upgrade in more detail

The Resource classification has incorporated all aspects of data quality, spatial distribution, geological and grade continuity, as well as estimation metrics (described as ‘kriging variance, kriging efficiency and slope of regression’).

An interesting factor to consider is that only mineralisation shallower than 300 metres vertically below surface has been classified as a Mineral Resource. This is due to the fact that material deeper than 300 metres is unlikely to support open pit mining.

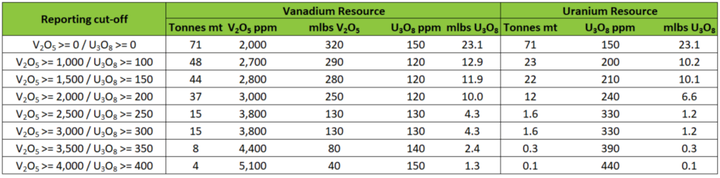

The below table shows the May 2018 grade tonnage data, all tonnes data expressed as millions of tonnes:

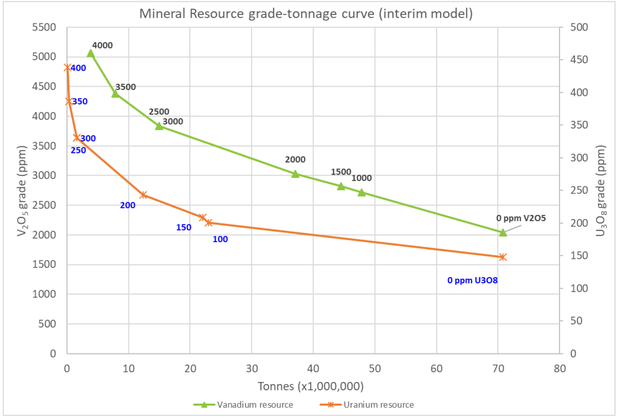

And below you can see the updated Daejon Interim Resource V2O5 and U3O8, grade-tonnage curves:

The previous vanadium estimate was for a very restricted area. Within this restricted area, the 2018 estimate predicts 21% more tonnes and 11% higher grade at a 2,000 ppm V2O5 cutoff — this could be ascertained via the 2018 p-XRF work demonstrating greater vanadium continuity.

However, as far as uranium goes, the story is a little different. The previous uranium estimate was based on down hole gamma equivalent U3O8 grades and the five SHK holes which provided a combined total of 1,179 samples to inform the estimate.

Keeping in mind not all the drill holes have been tested by p-XRF yet, and based on the currently available dataset, the 2018 estimate reports 41% less tonnes and 25% lower grade, compared to the 2013 Mineral Resource.

There are two reasons for this, one being the absence of some of the p-XRF data that’s still in the process of being collected, and the second contributing factor is a positive and rather obvious one — the enormous increase in available uranium from the new Estimate.

Next moves at Daejon

POW and Stonehenge have plenty planned for Daejon in the wake of the JORC upgrade.

It’s more immediate next steps will include selective flotation and magnetic separation test work, with the aim of beneficiating the vanadium grade by a minimum per cent.

Looking at beneficiation pathways used in the processing of Chinese ‘stone coal’, this form of beneficiation has successfully been used to upgrade V2O5 grade within shale/sediment hosted deposits by 4-5 times, and on average achieve a 300% upgrade...

In addition, POW is waiting on results of test work targeting the production of high purity, VRFB electrolyte grade V2O5 of greater than 99.5%.

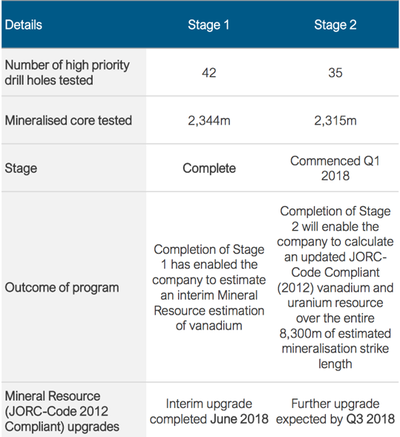

The company will also will complete Phase 2 assaying, targeting the remaining 60% of the known mineralisation strike. Tabled below are the details of Stage 1 (complete) and Stage 2:

And from there, POW will have its sights set on an updated MRE over the entire Chubu shale horizon captured within its tenements.

Of course, POW still has a lot of work to do to meet all of its goals, so investors should take all publicly available information into account if considering this stock for their portfolio.

Battery factory JV with DST Company Limited progressing well

While POW has a 50% stake in Stonehenge Korea (SHK) — the holder of the Daejon multi-mineral project — the other 50% stake is held by DST Company Limited.

DST reinstated on South Korea’s stock exchange a few months ago, thereby boosting the value of POW’s shareholding in its joint venture partner.

It is through this JV that POW lays claim to a part share of a battery factory in South Korea that gives it an end-to-end production to processing pathway.

The JV is looking to capitalise on the project through a $120,000 grant, taking the opportunity to fast-track the development and testing of its V-KOR range of vanadium redox flow batteries— specifically the 5kW/100kWh vanadium V-KOR batteries currently being trialled in Western Australia.

In June, POW provided an update regarding the extensive testing program carried out on its 5kW and 25kW V-KOR vanadium battery units, as covered on Finfeed.com (a related entity of S3 Consortium):

The company reported that over 3,000 cycles had been tested on the 5kW stack, representing in excess of nine years of full daily cycles for a typical solar photovoltaic (PV) application. In addition, more than 1,000 cycles (three years of full daily cycles) of testing has been completed on the 25kW stack.

Crucially, both units reported no significant degradation in performance...

The completion of the highly successful testing is considered to show “in use” high performance and thus marks a key step in POW’s progression towards the commercialisation of V-KOR batteries.

Both V-KOR units were independently tested by Korea Conformity Laboratories (KCL), a leading state-of-the-art national testing laboratory established over 40 years ago.

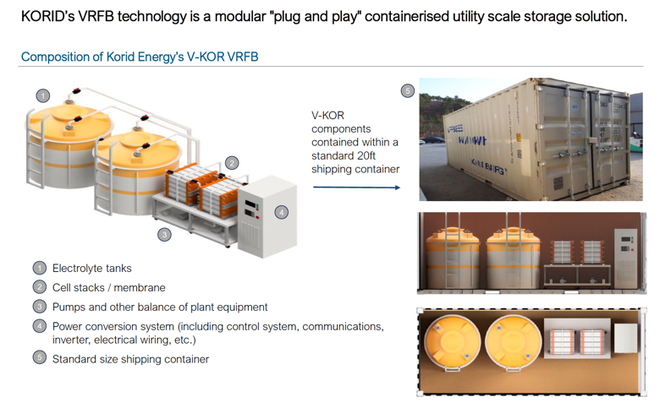

For a bit of background, this battery — a competitor for lithium-ion batteries, to supply the emerging massive huge market for renewable energy storage — is a modular ‘plug and play’ containerised utility scale storage solution:

VKOR is a commercial-ready solution, built-to-order for commercial, industrial and grid-scale applications, and has been designed by the JV to be fully scalable.

VKOR can provide from 2kW to 20MW and larger to suit specific customer requirements.

A quick look at the market

POW has its paws stuck into a true ‘coming of age’ metal, vanadium, and has secured a position in the enviable region of South Korea.

This is a particular advantage for the company, with its sights strategically set on the South Korean domestic vanadium market — totalling about 17 million pounds per year via offtake supply agreements through a strategic Korean partner.

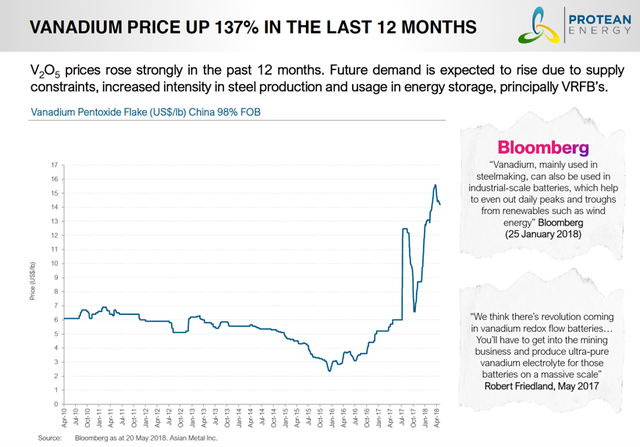

Meanwhile, vanadium has increased in price by a whopping 137% in the last 12 months:

The metal is currently sitting at around an eight-year high.

Although commodity prices do fluctuate and investors should seek professional financial advice for further information, if considering POW for their portfolio.

The China Iron & Steel Research Institute said a few months ago that the revised requirements for the standard tensile strength of rebar products in China could increase vanadium consumption by 30%, or 10,000 tonnes per year.

All in all, and primarily in light of today’s news, POW look to be in an excellent position to create some serious value for shareholders via its stake in the Daejon project.

It has been ensuring it is involved in exploration for appropriate vanadium deposits, while at the same time has its play downstream with its part stake in a V-KOR battery factory utilising advanced vanadium redox flow battery technology.

This is the first Australian commercial V-KOR vanadium battery deployment being tested in a micro-grid setting.

POW’s particular mineral assets (via SHK) are unique sediment hosted vanadium deposits, which means the potential to produce the high-purity vanadium pentoxide (V2O5) ideal for vanadium redox flow batteries.

Not to mention, it has defined a uranium Resource of 12.4 Mt at 240ppm U3O8, which doesn’t hurt either.

POW reported this week that it has A$3.1 million cash on hand... and A$1.9 million in listed securities.

Considering it’s one of just a few small caps on the ASX for those wanting to invest in an early stage future vanadium producer, we can see the opportunity for a whole lot of upside for this sub-$10 million capped junior.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.