Can this ASX Micro Cap Reshape NSW Gas Supply with Looming Offshore Exploration Campaign?

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Sydney may not be immediately aware, but the price of gas is about to start its upward journey .

The rise is occurring because LNG plants in Queensland are sucking up all the gas and selling it to Asia.

That wouldn’t be too much of a problem if the LNG operators weren’t dipping into the domestic market to find their gas.

In fact, it wouldn’t be too much of a problem if there was more gas to be extracted from NSW.

There is, but the gas isn’t making it out of the ground because the groundswell of local and political opposition to the coal seam resource has had its own ramifications.

So, what’s a state to do?

The company we’re focusing on today invests into exploration companies targeting potentially large energy and mineral resources and may have a solution to this current gas problem. This company, which recently opened and extended a Share Purchase Plan , has ambition to be one of the only gas players to look offshore NSW – where there’s no locking the gate.

Through an investee company, it has secured a vessel to start a seismic program to assist target drilling for natural gas in the hope of easing the looming gas burden.

The target is adjacent to Australia’s most populous region and the petroleum licence has the potential to hold 944 million barrels of oil equivalent as Prospective Resources of Natural Gas.

It is a region State and Commonwealth governments are keen to develop in order to unlock industrial users who may need a reliable supply of gas.

Remember, however, that this is an early-stage company still in the seismic phase, so it does have a while to go before taking advantage of the ripe market conditions – seek professional advice when considering this stock for your portfolio.

The company also recently signed a Letter of Intent (LOI) for potential supply of gas, but where this play really grabs attention is in a now-defunct government scheme which makes earnings on this stock free from capital gains tax.

When this company was awarded Pooled Development Fund status by the Federal Government it meant most shareholders didn’t have to pay tax on capital gains and dividends.

How does that work? Read on to find out.

But before you do, consider this:

This stock, currently capped at just $6.5M, is hedging its bets on two very different sectors: energy, and biotech.

If its imminent seismic programme bears fruit, and the Australian biotech sector experiences the kind of surge in market interest that its US cousins have received in recent years, then this company’s investments could quickly gain market traction on the ASX.

The company has a stake in a currently unlisted biotechnology player, which is showing excellent results in developing a pre-clinical model that can influence the development of liver cancer. That particular company could be listed on the ASX – providing an immediate look through value on what this company is holding.

It’s also taken a position in a technology that could assist anaesthetists to ensure patients remain properly sedated...

We’ll get to that later, but for now...

Introducing:

![]()

An Introduction

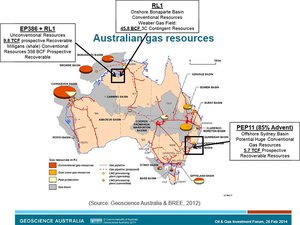

MEC Resources (ASX:MMR) holds interest in a company known as Advent Energy (with a controlling 44.29% stake).

Advent is looking at two gas projects on either side of the country.

Offshore, Advent is in a joint venture with Bounty Oil & Gas (ASX:BUY) on the PEP 11 permit – which is in the offshore Sydney Basin.

The demand side for Advent to develop that project is hotter than hot as they could influence the current gas crisis.

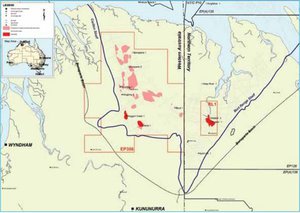

Meanwhile, Advent has a couple of permits close to the NT/WA border which are ideally located in one of the northern Australia development hotspots.

As you can see, it’s throwing around some large numbers in terms of the potential resource in play. Just look at PEP 11 in the above map: 5.7 TCF Prospective Recoverable Resources is impressive as are the numbers at RL1 and the EP386.

In order to fund the preparatory work for Advent’s seismic survey offshore the Sydney Basin (permit PEP11), MMR currently has an SPP open now, aimed at eligible shareholders at an issue price of $0.037 per share.

The SPP has been extended to 23 May 2016 , with shares expected top be issued on 26 May.

One of the more unique things about the $6.5M capped MMR is it is essentially set up as an investment company – and has its fingers in a lot of pies – from oil and gas... to biotech.

With this diversified strategy, any one of these could see this stock improve its value from its current low base...

Biotech, did you say?

MMR has a holding in BPH Energy (ASX:BPH), which in turn has an investee company known as Cortical Dynamics .

Cortical has developed an anaesthesia monitor, which recently received TGA certification and CE marking giving it the ability to market the equipment in Australia and Europe.

Cortical’s core product is the Brain Anaesthesia Response (BAR) monitor. The monitor improves on currently used electroencephalogram (EEG) technologies by incorporating the latest advances in our understanding of how the brain’s rhythmic electrical activity, the electroencephalogram (EEG), is produced.

This isn’t the only biotech play that MMR has though...

MMR also has a 20% holding in unlisted Molecular Discovery Systems (MD Systems) – which is attempting to develop a way to combat liver cancer.

MD Systems could be listed on the ASX and has been spun out of BPH.

MD Systems launched in 2006 with a main focus on drug discovery and validation of biomarkers for disease, therapy and diagnostics.

While oil and gas, through MMR’s holding in Advent Energy, is the main game here given the near term catalysts, the biotech holdings give it a greener tinge and could help diversify MMR’s interests and revenue streams.

No tax is good tax

The most interesting thing about MMR from an investment point of view is that most investors investing in MMR can actually have capital gains tax waived.

This is thanks to a now defunct program known as the Pooled Development Funds Program, which was available to some small to medium enterprise investors to encourage people to invest.

The Funds Program was available at the time MMR was first conceived, and even though it was subsequently scrapped for new entrants, MMR is one of the few companies which still receive that treatment.

Gains on investment in MMR are free from capital gains tax and investors will pay no income tax on dividends MMR may put out.

Suffice to say, it’s one of the more unique opportunities out there for investors looking for resources and biotech exposure.

Speaking of exposure, MMR has exactly that – to some of the more riveting demand side growth in Australian gas circles.

The importance of PEP 11

Generally when you think offshore oil and gas, you think of the big boys in the North West Shelf or the Bass Strait – you don’t necessarily think offshore NSW as a major petroleum province.

Yet, MMR believes there could have been offshore oil and gas there the whole time. The Sydney Basin is a proven petroleum basin.

MMR through its investee Advent assumed operatorship of the permit back in 2008, and since then has focused on compiling a suite of geo data (geological, geophysical and geochemical) to help it come up with a multi-TCF resource estimate.

So far MMR has observed sea surface slicks and thermogenic hydrocarbon seepage – in layman’s terms there’s oil slicks literally on the surface of the water and gas bubbling from the seabed.

It also drilled the New Seaclem-1 well on the permit back in 2010 – and while that well didn’t bring up gas it did offer the joint venture a lot more information on the rocks under the seabed.

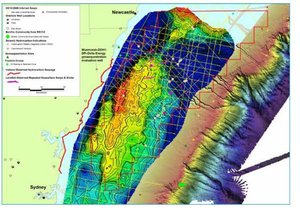

Below is a map representative of the seabed, with the red and yellow parts key structural highs – typically locations where gas and oil may accumulate.

It’s one thing to do seismic, but it’s quite another to drill into the actual rocks.

However, with the technical detail in hand, the price of oil collapsed and the joint venture Advent is part of decided to cool on the plan.

But, the rocks don’t change, and now the joint venture thinks it’s ready for another crack – having good reason to re-look at a target originally identified, but never drilled, by Santos & Ampolex 30 years earlier.

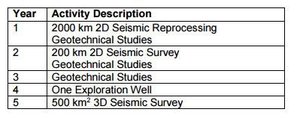

It’s just contracted a seismic vessel to conduct a 200 line km 2D seismic survey targeting Baleen – about 30 km south east of Newcastle.

This seismic is part of a five-year work commitment agreed to by the joint venture with the Commonwealth Government; MMR also recently received commitment to push the Seismic back until August 2016.

As you can see MMR and Advent are smack-bang in the middle of year two – and while the joint venture can seek variations to the work program, this will generally be the order of things.

The Commonwealth Government will be desperate for the JV to prove up a resource here – and so will the NSW government.

NSW – the state of play

Those on the eastern seaboard may be well aware of the imbroglio surrounding coal seam gas and the LNG industry.

An alliance of green groups and farmers have effectively blocked the development of CSG projects in the state, with the farmers fearing land contamination and green groups making a broader point about coal.

Regardless of whether or not coal seam gas simultaneously depletes and poisons the water table, the opposition to the industry in key marginal seats has meant the NSW political system has all-but ruled out development of the industry in the state.

That’s not great news for industrial users of gas in the state including chemical, metals and steel and manufacturing industries among others are facing shortfalls.

The whole reason the likes of Metgasco, Dart Energy, and AGL were pursuing projects in the first place is because of a massive expected shortfall of gas on the eastern seaboard – and NSW is sensitive to that.

Invariably, due to a pipeline network on the eastern seaboard it doesn’t really matter where the gas is generated, but for NSW a lot of the gas is generated outside of the actual state.

It’s generated in places like Cooper Basin in South Australia or Bass Strait, but here’s the strange thing.

Neither of these basins were expected to feed the massive LNG projects in Gladstone, Queensland.

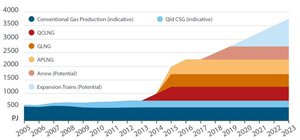

As you can see, the sheer demand created by the construction of QCLNG, GLNG, and APLNG for a start has the potential to have a distortive effect on the market.

It would have been less if CSG supplies in Queensland were able to be produced quickly enough to feed the projects, but the project proponents have found themselves needing to dip into the domestic gas market to feed the insatiable demand of the LNG plants.

These plants are tied to the Asian gas market, which buys gas at a premium, so the LNG players are simply able to outbid local industrial users of gas.

The ACCC recently put out the findings of an enquiry it was holding into the east coast gas situation – looking at whether anything could be done to alleviate the gas crisis by seeking to understand whether gas suppliers were acting unscrupulously in the market.

It made some rather unremarkable conclusions.

The ACCC found most industrial users in the southern states were forced to deal with the Gippsland Basin Joint Venture, which is a 50-50 joint venture between Esso and BHP Billiton – the biggest producers of gas out of the Bass Strait.

So, instead of dealing with two parties and all the competitive advantages that implies for users, the users have to effectively deal with a monopoly.

In its conclusions, the ACCC found that users were stuck between a rock and a hard place.

“The gas users in these states are becoming overly dependent on the jointly marketed GBJV gas,” it said.

“If their alternative to dealing with the QBJV is to transport gas from Queensland, southern users may have to pay considerably more for gas than they are otherwise likely to pay in a competitive market.”

The solution seems pretty obvious.

“There is a need for more sources of gas supply, particularly in the southern states,” the ACCC said.

Enter MMR

The ACCC went on to urge the government not to adopt blanket coal seam gas moratoria, but politically speaking, that’s not likely.

CSG has become a toxic issue in NSW politics, and the party which steps up to the plate to try and secure more supply within NSW from CSG will more than likely be shouted down.

There are, however, no alliance of farmers and green groups in the ocean – and this is where MMR can do something good for the gas market.

There’s no gate to lock at sea.

If MMR is able to prove up a gas resource just off the coast of NSW, then it will well and truly be off at the races.

Because LNG players have been dipping into the market, the price differential between the traditionally lower domestic price and the higher Asian price has narrowed.

This means that in the future, a domgas (domestic gas) play is likely to be more profitable.

We should note again that MMR is still in the early stages of exploration here, so seek professional advice if considering this stock for your portfolio.

MMR could be on pretty fertile ground then, in more ways than one.

EP386 and RL1

Over on the WA/NT border, MMR has its feet on two projects.

They lie in an area known as the Bonaparte Basin, which is Australia’s third most prolific proven petroleum basin but has remained lightly explored onshore.

We’ll get to why in a moment, but we’d like to tell you a little bit about what MMR is looking at in particular.

The conventional

Both permits have conventional (stick a drill in the ground and away you go), and unconventional (reservoirs need to be stimulated to flow) potential within them.

On the conventional side, gas discoveries have never really been commercialised.

The main game at EP386 are the Vienta, Waggon Creek, and Bonaparte plays and contain an estimated recoverable resource ranging from 53.3 billion cubic feet to 1.3 trillion cubic feet.

Not bad.

What’s better is that wells targeting the conventional have been drilled before – and they’ve been put under production test. In fact, over the course of the journey there have been nine drilled in the permit.

This isn’t wildcat country – in fact, here’s Waggon-1 being flared:

The well was drilled back in 1995, but production testing of that well in 2012 demonstrated flow of over 1 million cubic feet of gas per day from a 217m gas column.

Another well drilled in the permit, Vienta-1, flowed at 2 million cubic feet of gas per day.

Meanwhile over in RL1, MMR has its foot on the Weaber gas field.

The field was discovered back in 1985, but never put into production. Back in 2011, Advent undertook a review of all the available data and essentially re-mapped the field.

After that, it commissioned an independent assessment for the field which found the Weaber field could have a contingent resource from 11.5 billion cubic feet of gas to 45.8BCF. Not export LNG-scale stuff, but at least worth following up on.

The long game at both permits is the unconventional.

Unconventional

The unconventional potential of the Bonaparte Basin has always been a hot talking point – as of a lot of shale has shown up while drilling conventional wells.

Thanks to the unavailability of equipment in the area though, it’s never really been tested too much with the drillbit.

The best people have been able to do is measure the shale, and then take recordings of it, and send it off to independent assessors.

One such outfit is the Australian Council of Learned Academies (ACOLA), which has put the unconventional potential of MMR’s play region at 6 trillion cubic feet of gas recoverable.

That’s big – but it also doesn’t begin to tell the real story.

You see – ACOLA took a shale thickness figure of only 36m. Advent, on the other hand, thinks there could be as much as 300m to 1500m of shale thickness in the permits.

So, you can imagine what that may do to the numbers.

Advent has put the unrisked gas in place figure at between 19TCF to 141TCF, with a risked recoverable figure of 9.8TCF.

The other thing ACOLA did to be prudent was use a total organic content figure of 1.8%, but analysis of previous drilling has made Advent declare that this figure could be up to 5%.

The unconventional is the huge prize here – but for an unconventional play in Australia to fly you need a lot more than just prospective rocks...

NT development

One of the more frustrating things about the shale gas scene in Australia is that its rocks are so good.

If Australia had its act together, we could see a US-style shale gas revolution taking place.

Unfortunately, it takes more than just rocks to make a shale play successful.

It takes markets, equipment, and customers.

To date, unfortunately, those things have been lacking for players in the Northern Territory and northern WA.

But, there are signs that this could be about to turn around.

On the WA side of the border, there’s an overarching economic plan to unlock the value of the Ord River...

The video demonstrates the value the WA and federal governments are trying to unlock along the Ord River, which runs from Lake Argyle out to the sea – through Kununurra.

The program is being run through the WA state’s Royalties for Regions program – with an estimated $515 million spend on the project (about $300 million from the program, the rest from different sources).

It basically involves opening up irrigation channels along the Ord, along with developing several common-use infrastructure projects. In doing so the Government has now built a highway right into Advent’s permit allowing for the project to be developed.

The first point is to generate a lot more farming land to fuel the so-called ‘dining boom’ – but where MMR can play a role is with the industrial development which comes along with it.

After all – industry needs gas.

MMR has taken the first step in this, although it doesn’t directly concern the Ord scheme.

Back in March MMR tied up a non-binding letter of intent with Northern Minerals (ASX:NTU) for the supply of gas to its Browns Range project.

The LOI spells out the terms and framework for ongoing discussions for gas supply.

The LOI is non-binding so don’t take it as an iron-clad guarantee that a deal will eventuate and apply caution to your investment decision.

Still, it’s a sign of the type of deals MMR could seek to do in the space if more industrial gas users came to the party.

More industrial users are expected to come to the party if the Federal Government has any say about it. The project could have the potential for export LNG and is within 70 km of pipeline and port infrastructure.

Both sides of politics have long talked about the potential of northern Australia as one of the last great development projects left in Australia – and the evidence of that is in the Northern Australia Infrastructure Bill 2016.

It’s a sign that talk is on the road to becoming reality – a senate committee labelled it a “new approach to tackling the economic and social issues which have plagued Northern Australia for over 100 years.”

Suffice to say, it’s being read as a pretty big deal.

The government is thinking of tipping in $5 billion into an infrastructure fund to get the territory rocking.

After all, northern Australia has 40% of the land mass but contributes to just 11% of GDP – there’s scope for catch up here.

The $5 billion will come in the form of a loan program to fund things like airports, roads, rail, energy, water, and communications – all the things industry needs to make their operations a reality.

Just image then, being a small gas player which is aiming to prove up a huge gas resource in the region...

New market studies have identified a current market demand of up to 30.8 TJ per day of power generation capacity across the Kimberley region that could potentially be supplied by MMR’s conventional gas projects in EP386 and RL1.

In addition, the Federal Government’s White Paper on Developing Northern Australia described an estimated increase in electricity consumption of 52% by 2018 for northern Western Australia.

The massive problem which has plagued the region’s upstream gas explorers in the past is that there hasn’t been the commercial weight at play to allow the gas resource to make it to surface – in short, there haven’t been a lot of customers in the region.

Just imagine there’s a massive redevelopment which lures new players to the region – you’d think they may want to lock down a sustainable source of gas before they get there...

The Final Word

All in all, while MMR remains an early-stage play, it is at least one of the more interesting ones out there.

MMR’s investment in Advent Energy means it is strategically placed in two of the emerging gas stories in Australia.

In NSW it is well-placed to take advantage of a gas shortage which will start to bite in the coming years, and in the Northern Territory it is in the exact right spot to take advantage of one of the largest infrastructure projects the country has ever seen.

Combine all that with its status as a pooled investment and you have a play which is worth taking at least a second look at.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.